How to Get a Virtual Dollar Card in Kenya for Online Payments

[Photo/Courtesy]

For a professional or an advanced user of financial tools in Kenya, access to dollar payments stopped being optional a long time ago. Currency market restrictions, CBN policies and the regulation of external FX flows make direct access to USD essential for paying international services.

A virtual USD card lets you do more than pay for subscriptions and SaaS used by global companies. It also gives you control over the payment infrastructure of your business or freelance work. Having such a card becomes a strategic tool for managing personal and corporate finances under currency instability and global integration.

What types of virtual USD cards are available in Kenya

Local Kenyan FinTech services

Local fintech platforms issue cards through partner banks and use BINs supplied by licensed international issuers. The main constraints come from transaction limits, daily and monthly top up ceilings and the liquidity of FX reserves.

A practical note: before choosing a service, check its limits for international transactions and whether it supports multi currency wallets that convert naira to USD automatically. This reduces FX risk.

International platforms that work with clients in Kenya

International issuers differ in their KYC demands. Some require strict identity and address checks, others rely on basic identifiers. BIN differences (UK, EU, US) influence how the card behaves with various merchants. Some merchants block cards from certain regions or apply a wider conversion spread.

For a professional, assessing BIN type in relation to the merchants you plan to use is essential. It lowers the chance of failed transactions and avoids delays due to refunds.

Virtual cards issued by digital banks

Cards linked to multi currency wallets follow a different architecture from classic virtual cards without an account. They let you manage FX reserves through an API, provide reports on conversion and fees and allow instant creation of additional virtual cards for different tasks.

For business users, this gives flexibility in managing payment infrastructure and reduces reliance on physical bank accounts.

Requirements for issuing a card: what to prepare in advance

To request a card, you must provide the necessary documentation, typically including a national ID or passport along with proof of residence such as a recent utility bill or a bank statement. Any mismatch between your name and address on these documents can lead the card issuer to delay processing or even decline the application.

Banks and fintech providers often impose additional requirements: for instance, maintaining a minimum account balance or linking the card to a local bank account to facilitate accurate NGN to USD conversions. By gathering and verifying all required documents beforehand, you significantly reduce the likelihood of rejections or administrative delays

How to choose the best virtual USD card: top 5 card providers for Kenyan residents

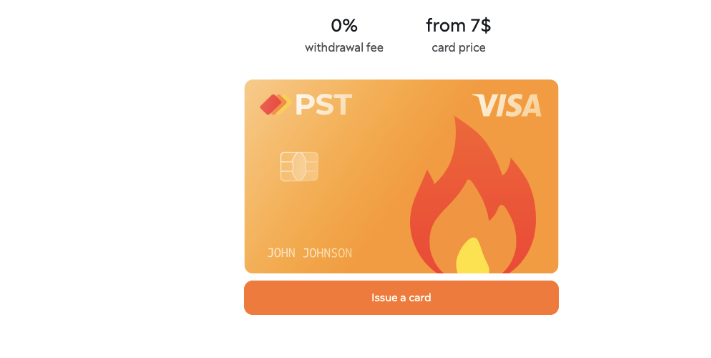

1. PSTNET

PSTNET is an international fintech service that provides virtual payment cards, including its versatile Ultima card. Because the platform supports both Visa and Mastercard, the card operates the same way as a regular bank-issued card. But such virtual dollar cards allow easy high value purchases, flight bookings or hotel reservations from anywhere.

How to get the card:

To obtain the Ultima card, you create an account on PSTNET. You can sign in using Apple ID, Google, Telegram, WhatsApp or email. Then you complete a short KYC step that only requires a passport. After that, you top up your deposit through any convenient method and open the card in your dashboard. You can create as many cards as you like.

New users can deposit their first USDT amount with zero fee. Seventeen more cryptocurrencies are supported, along with bank transfers and transfers from Visa or Mastercard. Top up fees start at 2 percent. There are no withdrawal fees.

A mobile app is available for Android and iOS.

Support is available 24/7 through the dashboard chat, WhatsApp and Telegram. Telegram also offers updates and service notifications.

- Price: weekly plan 7$ or annual payment 99$ (currently a 48% discount applies)

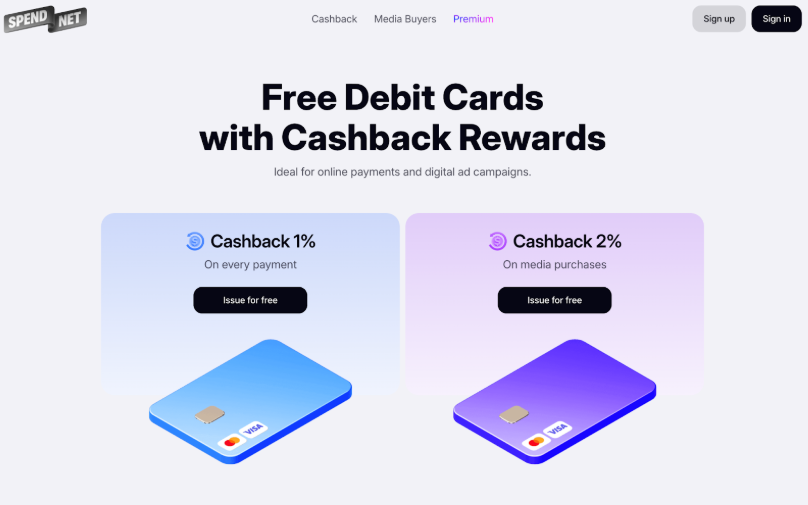

2. Spend.net

Spend.net offers virtual dollar cards with cashback. Its cards return 1 percent on any purchase. Since they run on Visa and Mastercard, they work across a wide range of international online platforms.

There are also specialised cards with 2 percent cashback for advertising spend. There are no limits on the number or type of cards. Users can issue as many as they need.

How to get the card:

To issue a 3D secure virtual dollar card on Spend.net, you create an account using Google or email. Then you complete the mandatory KYC step. Verification takes little time.

Deposits can be made with USDT (TRC20, ERC20) and BTC. The user sets the fee. The higher the deposit, the lower the fee. The minimum is 2 percent. Withdrawals are free, as are many other key operations.

There are no fees for card issuance.

Cashback is earned automatically and can be monitored directly from the user dashboard.

Customer support is accessible through the platform’s chat feature.

- Price: 0$

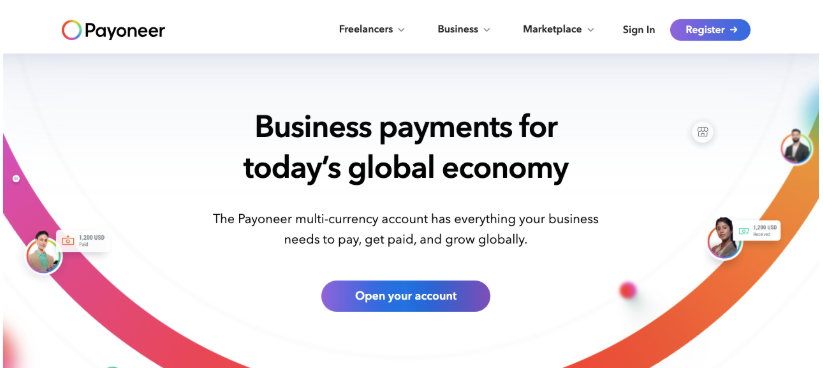

3. Payoneer

The well known fintech brand Payoneer issues virtual cards on Mastercard. The key feature is multi currency support. Cards can operate in USD, EUR, GBP and many others, including Kenyan naira. The service mainly works with businesses. Payoneer cards allow users to receive payments from international clients, convert currencies and pay online wherever Mastercard is accepted. Plastic cards are also available.

There are no limits on the number of cards, and they can be issued instantly. However, spending is limited: one card can process up to 200,000 USD per day.

How to get the card:

Since the platform is built for global businesses and start ups, registration requires the company name, phone number, email and country. Kenyan companies are supported.

After registration, you verify your identity with documents. Deposits can be made using crypto, bank transfers and internal transfers between Payoneer users. Top up fees vary but do not exceed 4 percent. Internal transfers are free. Withdrawals to local bank accounts are available with fees starting at 1.50 dollars.

Internal currency conversion carries a fee, usually about 3 percent.

The first card costs 29.95 dollars. All additional cards issued during the year are free. However, if your account receives less than 2,000 USD per year, the service charges another 29.95 dollars as an annual penalty.

- Price: 29.95$ for the first card, subsequent cards free

4. EzzoCard

EzzoCard issues prepaid cards with fixed balances. You can choose Visa or Mastercard with values from 10 to 2000 USD. You do not need to register. You simply buy a card on the website. This works for one time purchases or gifts. The main advantage is full anonymity, but this also means limited features and weaker security.

How to get the card:

You do not need registration or KYC. Choose the card value and pay online using any of nine cryptocurrencies or services like PerfectMoney or WebMoney.

The price includes the value loaded on the card plus the platform fee. For example, a 10 dollar card costs 16.99 dollars. A premium gold card worth 2000 dollars costs 2240.99 dollars. After payment, the card is delivered by email. Each card has its own validity period, from 7 days to 12 months.

There are no limits on quantity. Withdrawals are not available, as these cards are non refundable.

Support is available by email during business hours.

- Price: 6.99$ to 240.99$ depending on value, type and expiry

5. Raenest

Raenest is an emerging fintech startup focused on serving both individuals and businesses across Africa. The platform specializes in issuing virtual USD cards on the Mastercard network. With Raenest, users can easily convert USD into NGN or other local currencies, make purchases and transfer funds to other Raenest users instantly.

In addition to virtual cards, Raenest also offers physical card options, giving you flexibility depending on your spending needs.

How to get a Raenest card:

You can either sign up through their website or download the Raenest mobile app. Then you’ll need to submit a selfie along with a valid passport or government-issued ID, and provide your phone number, email, and full legal name. Once your KYC verification is completed, you receive full access to the platform, unlocking all its financial tools.

Issuing a card is just as intuitive. After selecting your preferred card type, you pay around $3. You can then configure your card by setting spending limits and choosing the preferred payment currency.

Top ups can be made through bank transfers or payments from Visa or Mastercard. Each top-up carries a nominal $0.50 fee.

- Price: 3$

Navigating USD card issuance in Kenya: a step-by-step guide

Step 1: Identify your funding source

Compare bank conversions, crypto gateways and P2P platforms by cost, speed and reliability. Timing matters for reducing losses due to spreads and volatility.

Step 2: Prepare KYC with Kenyan specific issues in mind

Make sure your documents match the issuer’s standards. Address verification and mismatched names are common reasons for rejection in Kenya.

Step 3: Pass the issuer’s risk sandbox

New cards go through extra checks during first transactions. Errors in user data, frequent high value attempts or unusual merchant types can trigger a soft ban.

The professional approach is to test the card with small payments and increase volume gradually.

Step 4: Test the card with different merchant types

Try it on SaaS platforms, ad accounts and educational services. This reveals BIN restrictions and FX spreads early, letting you adjust your plan.

Step 5: How to switch to a new card without losing subscriptions

When changing cards, move all recurring payments. Use an overlap period where both old and new cards stay active. This keeps subscriptions from failing due to declined authorisations.

To sum up

A USD card becomes part of your personal and corporate payment infrastructure. It provides stable access to global platforms, reduces FX risk and increases financial mobility. It lets you operate independently from local restrictions and integrate into global payment ecosystems.

FX reforms and new licences for payment providers will change how accessible USD cards are. Cards will integrate with UK and EU rails, and user risk segmentation will become stricter.

Professionals should factor this in when choosing a provider and planning their payment infrastructure to avoid delays and unnecessary fees.